Help First, Sell Second: A New Member Acquisition Playbook for Credit Unions

Credit unions spend an average of $442 to acquire each new member¹. Reaching low-to-moderate income households often costs even more. These households represent a massive market - 60% of Americans live paycheck to paycheck², but the traditional acquisition playbook misses them entirely. Ads for checking accounts and competitive loan rates don't land when you're facing a utility shutoff or choosing between rent and groceries.

What if the path to new members didn't start with a pitch at all? What if it started with help?

Starlight ran pilots in late 2025 testing exactly that premise: lead with free, proactive assistance, connecting people to utility relief, food assistance, childcare subsidies, and other benefits they're already eligible for, and let the credit union relationship grow from there. No upfront sell: just genuine help, delivered through the credit union, before any product conversation begins.

By adding benefits navigation to their product stack, credit unions create a relevant entry point for households traditional acquisition couldn't reach, and earn trust before asking for it.

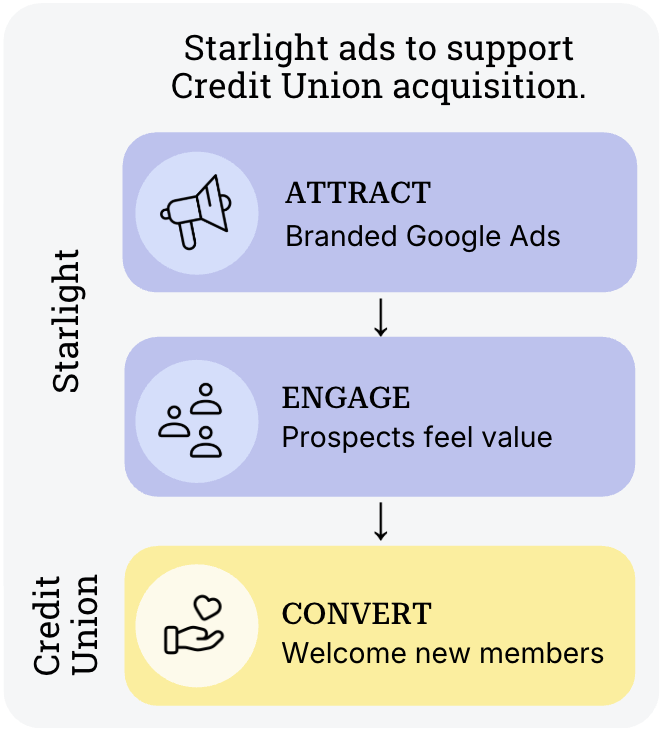

How the Pilots Worked

Campaigns targeted people actively searching for utility assistance, rent help, childcare programs, and food assistance. When someone clicked, they landed on Starlight's benefits navigation tool: enter basic information and instantly see programs you qualify for, ranging from $2,000 to $7,000 annually giving households real financial relief.

The platform provides step-by-step application guidance for each program. The warm hand-off join the credit union that just connected you to thousands in support.

The Results

Lead costs dropped to $10-16 (industry benchmark: $75-1303). Estimated cost per member fell to $45-80, nearly 90% below the industry average of $4421.

The conversion rate held because people searching for utility assistance or rent help are high-intent-they need help immediately:

- In the St. Louis pilot, a mother searching for down payment assistance discovered she qualified for a $7,000 grant, $600 in utility relief, and local food bank access. She joined the credit union because it mapped a path to homeownership while solving immediate needs.

- In Detroit, a veteran on quarterly 1099 income assumed irregular earnings disqualified him from assistance. He learned SNAP assesses eligibility on a 30-day window-he qualified during months between payments for $292 monthly, plus $800 utility relief and $1,000 in one-time stability funding. He joined because the credit union explained resources no one else had.

- In New York, a resident discovered $800 toward heating costs through an energy assistance program and joined because the process was simple and the benefit was immediate.

Lead costs stayed low initially - $10-15 - then climbed toward $15-20 as campaigns scaled to broader audiences (Auction saturation occurs as we spend more but can continue to manage towards your internal benchmark). Metropolitan areas see more available audience versus rural markets, but both stayed well below industry benchmarks due to a highly relevant product for the average resident.

The LID Opportunity

These campaigns do more than reduce acquisition costs - they build toward Low Income Designation (LID). By anchoring geographic targeting to the NCUA's defined LID areas, outreach can reach lower-income communities exactly where it counts, so member growth doubles as progress toward the designation.

As CUCollaborate explains, to obtain LID, "a majority (50% plus 1 member) of a credit union’s membership must be deemed "low-income members." A federal community credit union may also achieve LID if a majority of its potential membership qualifies as low-income. These members are identified based on U.S. Census Bureau data, with low-income thresholds set at 80% or less of the median family income or median earnings for individuals for their respective metropolitan area or the national metropolitan average, whichever is greater. For those living outside metropolitan areas, statewide or national non-metropolitan median family incomes or median earnings for individuals are considered instead."4

LID unlocks expanded business lending authority, non-member deposits, and operational flexibility that opens new markets. With acquisition costs under $100 per member and targeting anchored to qualifying LID areas, credit unions can make meaningful progress toward the majority-low-income threshold. By adding financial assistance navigation to their product stack, credit unions get both: affordable acquisition and a path to designation.

What Comes Next

Starlight is running pilots with credit unions across geographies to build a repeatable playbook: which programs drive engagement, how messaging shifts by region, what member retention looks like at 6 and 12 months.

The early pattern is clear: solve an immediate crisis before asking someone to join, and they remember. For credit unions trying to serve the households that represent most of America, benefits navigation provides the product stack that makes acquisition sustainable.

Join the Movement

Starlight is helping credit unions expand their impact by making financial assistance programs more accessible. Want to test this with your credit union? Email us at hello@get-starlight.com.

Click here to see the full case study

Footnotes

- The Financial Brand, cited in CUNA Strategic Services, "How Your Credit Union's Loan Strategy Is Silently Killing Growth" (2025). https://www.cunastrategicservices.com/content/how-your-credit-unions-loan-strategy-is-silently-killing-growth ↩

- Reality Check: Paycheck-to-Paycheck (2025); https://step.com/money-101/post/how-many-americans-are-living-paycheck-to-paycheck-in-2025 ↩

- Flyweel, "Cost Per Lead Benchmarks 2025" (2025); https://www.flyweel.co/blog/lead-gen-cpl-cac-benchmark-index-2025 ↩

- CUCollaborate, “Growing Credit Unions With Low Income Designation” (2024) https://www.cucollaborate.com/blogs/growing-credit-unions-with-low-income-designation-lid ↩

Published June 17, 2026